Guerra valutaria. Il corvo disse al merlo che era nero.

Giuseppe Sandro Mela.

2018-07-27.

Cercare di comprendere cosa stia succedendo al mercato mondiale delle valute è fenomeno di comprensione molto difficile.

*

Se da una parte sicuramente ben poco delle reali situazioni ed intenzioni è reso noto al grande pubblico, anche a quello usualmente bene informato, da altra parte capire cosa stia accadendo richiederebbe uno sforzo mentale davvero severo, che riesce a ben poche persone. Però tentare ne varrebbe la pena.

In primo luogo, il rapporto che intercorre tra due valute è determinato da una congerie di concause, alcune delle quali possono funzionare da trigger: è un complesso sistema multivariato, e per di più non lineare. La mente umana tende, si direbbe in via naturale, a cercare di semplificare i termini del problema, enucleando alcune regolette. Per esempio, che una valuta debole faciliti le esportazioni. Orbene, questa è una verità parziale, molto parziale: facilita le esportazioni che non abbiano contratti predeterminati di lungo termine, e solo per un breve lasso di tempo: poi iniziano i dolori di doversi rifornire di materie prime a costi aumentati. Il caso cinese è paramount: se è vero che un renminbi sottovalutato faciliti le esportazione sarebbe altrettanto vero che pesa come un macigno nell’import di energetici, dei quali la Cina è quasi priva. Si dovrebbe sempre diffidare dalle mezze verità.

In secondo luogo, il mercato valutario è influenzato in modo marcato da considerazioni politiche, le quali spesso antepongono questioni di principio a quanto la ragione suggerirebbe leggendo i dati di fatto. La Cina, per esempio, cerca di mantenere il renminbi debole rispetto al dollaro americano non solo per facilitare l’export in tale continente: la sua visione è globale e deve mandatoriamente tener conto, per esempio del progetto Belt and Road. Si tenga conto che, piaccia o non piaccia, mentre il politico può scatenare una guerra armata, un banchiere centrale deve solo adeguarsi alle politiche governative e non ha armi se non gli strumenti economici e finanziari. Spesso nella storia i conflitti armati hanno sancito nuovi equilibri, altrimenti non raggiungibili.

In terzo luogo, il mercato valutario tratta cifre enormi, che sfuggono la comprensione: il solo Forex scambia ogni giorno oltre 4,000 miliardi di dollari americani contro altre valute. Ma il Forex non è l’unico mercato. Questa sola cifra dovrebbe essere sufficiente per far comprendere come la maggior parte delle entità finanziarie siano impotenti di fronte al mercato valutario.

In quarto luogo, uno dei principali compiti delle banche centrali dovrebbe essere il mantenimento dei mercati dei cambi in una ragionevole stabilità. Con 4,000 miliardi trattati ogni giorno, una variazione dell’1% si concretizza in 40 miliardi: una cifra non da poco. I sistemi economici soffrono notevolmente a seguito di variazioni rapide dei cambi, e tutti gli oneri sono addossati al comparto produttivo e commerciale. In un’ottica globale, spesso ciò che si guadagna da una parte lo si perde dall’altra. Von Mises aveva definito questo fenomeno come eterogenesi dei fini.

In quinto luogo, le valute non sono ectoplasmi. Esse rappresentano grosso modo lo stato dell’economia della nazione emittente. Se è vero che il mercato valutario condiziona anche severamente nel breve il sistema produttivo, è altrettanto vero che sul medio lungo termine è questo ultimo che detta legge. È solo un problema di equilibri.

Nel ragionare sulle valute, si tenga sempre presente come in Cina al momento i consumi interni costituiscano solo circa il 35% dell’intera economia, contro un 70% circa nei paesi occidentali, in termini mediani. In altri termini, l’economia cinese dipende dal’export molto più di quelle occidentali. Ma non è la Cina che deve adeguarsi agli standard occidentali: è l’Occidente che dovrà adattarsi a quello cinese.

In sesto luogo, di questi tempi si sta assistendo ad un rovesciamento di molte visioni economiche. Le teorie fin qui usate hanno dimostrato di essere incapaci di descrivere i fenomeni in atto e, di conseguenza, di poter fare ragionevoli previsioni. In questa sede interessa constatare solo uno di codesti mutamenti. Molte teorie sostengono come i consumi interni determinino la buona salute del sistema economico, da cui le politiche a loro sostegno. Il caso cinese è la dimostrazione lampante di quanto ciò sia solo una verità estremamente parziale. Non a caso il cuore della dottrina economica del Presidente Trump privilegia la produzione nazionale, fatto questo vissuto negli Stati Uniti in modo conflittuale con la minoranza democratica.

*

Ciò premesso, possiamo adesso entrare nel cuore del problema attuale.

«Central bankers and finance ministers aren’t usually the ones who fight wars. But the global economy is a dangerous place, full of threats to prosperity. That’s given rise to the idea that there’s a tussle for competitive advantage going on, with each country brandishing its currency as a weapon. The standard view assumes policy makers are driving down exchange rates — or fixing them too low — so that goods made by their exporters can be sold cheaper overseas, providing a jump-start to the economy at home. When other nations retaliate, it ignites a currency war. Central bankers say they’re not trying to pick fights. Rather, they’re keeping a hold on interest rates or taking other steps to stimulate economic growth. That creates spillover, however, as money flees for countries with higher rates, pushing currencies upward and hurting exporters. Whether intentional or not, these unspoken currency wars still create peril — and real winners and losers.

The Situation.

President Donald Trump and other U.S. officials have accused China, Germany, Russia and Japan of gaining an advantage by keeping their currencies weak. Trade tensions were said to prompt China to consider depreciating the yuan as a tool in negotiations, after letting it gain in value against the dollar for several years. At the same time, Trump has been nudging the dollar lower as a way to increase exports, reduce the trade deficit and boost profits for multinational companies. Before these spats, the currency wars had simmered for years as countries fought their way out of the recession triggered by the 2008 financial crisis. As more central banks embraced unconventional monetary policies to protect their economies, the race to the bottom took on new momentum. The U.S., Japan and Europe used bond-buying plans in addition to rate cuts to stimulate their economies. Japan jolted markets by introducing negative interest rates in 2016, following the European Central Bank’s move below zero in 2014.» [Bloomberg]

*

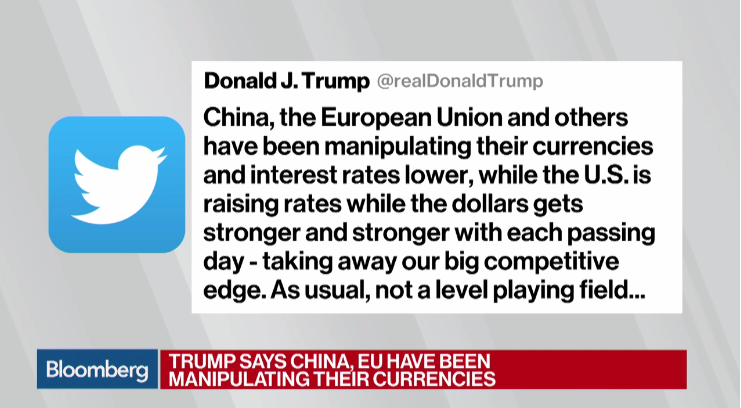

«President Donald Trump and other U.S. officials have accused China, Germany, Russia and Japan of gaining an advantage by keeping their currencies weak».

Questa è una scelta politica.

L’Amministrazione Trump si troverà a gestire due esigenze opposte e contrastanti. Da una parte la Fed per motivi di finanza valutaria avrebbe bisogno, e ne avrebbe tutte le intenzioni, di aumentare i tassi di interesse richiamando così valute sul dollaro, che si irrobustirebbe. Dall’altra parte Mr Trump vorrebbe che ciò non accadesse.

Nota.

Renminbi e yuan non sono termini equivalenti. Il primo indica la valuta della Repubblica Popolare Cinese, il secondo, che letteralmente significa ‘rotondo’, indica l’unità base di conto, suddiviso in dieci jiao a loro volta suddivisi in dieci fen.

– Trade fight spreads to FX as president talks down dollar

– Equities, oil, and emerging-market assets at risk from FX war

*

The currency war has arrived.

So say some of the best and brightest in the $5.1 trillion-per-day foreign-exchange market. U.S. President Donald Trump on Friday accused China and the European Union of “manipulating their currencies and interest rates lower.” The comments came after the yuan plunged to its lowest level in a year, with little sign of China’s central bank intervening to stem the slide. They also follow a decline in the euro this year and add to the calculus that European Central Bank policy makers might need to consider when they meet next week.

As the world’s largest economies open up a new front in their increasingly acrimonious game of brinkmanship, the consequences could be dire — and ripple far beyond the U.S. and Chinese currencies. Everything from equities to oil to emerging-market assets are in danger of becoming collateral damage as the current global financial order is assailed from Beijing to Washington.

“The real risk is that we have broad-based unravelling of global trade and currency cooperation, and that is not going to be pretty,” said Jens Nordvig, Wall Street’s top-ranked currency strategist for five years running before founding Exante Data LLC in 2016. Trump’s recent rhetoric “is certainly shifting this from a trade war to a currency war.”

China’s shock devaluation of the yuan in 2015 provides a good template for what the contagion might look like, according to Robin Brooks, the chief economist at the Institute of International Finance and the former head currency strategist at Goldman Sachs Group Inc. Risk assets and oil prices would likely tumble as worries about growth arise, hitting currencies of commodity-exporting countries particularly hard — namely, the Russian ruble, Colombian peso and Malaysian ringgit — before taking down the rest of Asia.

“Asian central banks will initially try to stem currency weakness through intervention,” Brooks said. “But then Asian central banks will step back, and in my mind, the big underperformer on a six-month horizon could be EM Asia.”

Whether the People’s Bank of China attempts to anchor the dollar-yuan exchange rate near 6.80 to avoid further escalation is key, according to Nordvig. He says ECB President Mario Draghi may elect to step into the fray at the central bank’s July 26 policy meeting, given American attempts to talk the dollar down in January were extremely unpopular in Frankfurt.

The Bloomberg Dollar Spot Index fell as much as 0.8 percent Friday, the most since March. The euro ended the day up 0.7 percent at $1.1724, while the yen was almost 1 percent stronger.

Treasury Secretary Steven Mnuchin said Friday that the U.S. is closely monitoring whether China has manipulated its FX rate, according to Reuters.

“There’s no question that the weakening of the currency creates an unfair advantage for them,” Mnuchin said. “We’re going to very carefully review whether they have manipulated the currency.”

The Treasury’s next semi-annual foreign-exchange policy report — the government’s formal channel to impose the manipulator designation — is expected in October.

The Department in its last report in April refrained from branding China with the label, but stepped up criticism of the Asian nation’s lack of progress in rectifying its trade imbalance with the U.S.

“The exchange rate is one of many instruments China could use” to counter U.S. tariffs, Joseph Stiglitz, the Nobel Prize-winning Columbia University economist and former adviser to President Bill Clinton, said in a July 17 interview. “They would make a big effort to say what they are doing is not motivated by that,” he added. “We won’t be able to clearly tell. We don’t usually know the extent of intervention.”

The greenback will likely continue to suffer as investors heed Trump and back out of long dollar wagers, according to Shahab Jalinoos, Credit Suisse Group AG’s global head of FX trading strategy.

Hedge funds and other speculators are the most bullish on the currency since February 2017, according to data released Friday from the Commodity Futures Trading Commission that tracks positions through the week ended July 17.

“It has now been virtually defined as a currency war by the U.S. president, given that he explicitly suggested foreign countries are manipulating exchange rates for competitive purposes,” Jalinoos said. “The barrage of commentary will likely force the market to scale back long dollar positions.”

Nessun commento:

Posta un commento